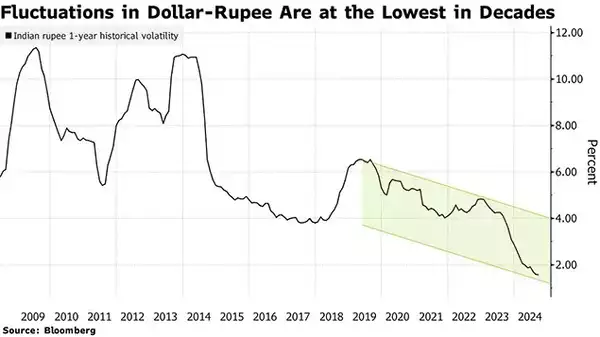

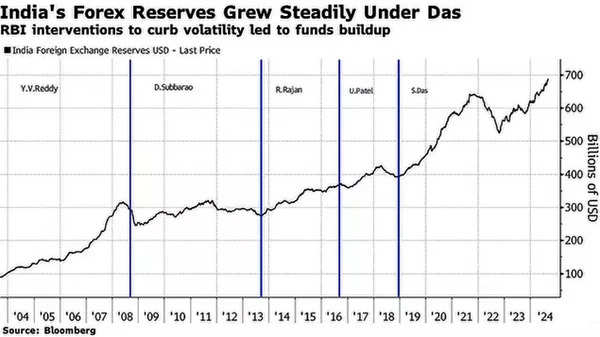

The RBI’s foreign-exchange reserves have swelled to almost $700 billion in a move reminiscent of China’s accumulation two decades ago. Frequent interventions under Das, whose six years in office are due to end in December, have transformed the rupee from Asia’s most volatile currency to one of the least.

At the same time, the exchange rate has dropped to record lows near 84 per dollar without sparking warnings about spiraling import costs and inflation.The latest example: The rupee’s move was comparatively slight when the Federal Reserve’s outsized interest-rate cut this week jolted global markets.

Clamping down on volatility and building up a stockpile of foreign exchange holdings to safeguard the economy in the event of skittish overseas investors pulling funds has been a key plank of the RBI governor’s tenure. While the strategy has helped attract foreign investment and improved a current account deficit that often caused headaches for Das’s predecessors, the interventions also bear risks and have been censured by the US Treasury.

Das had some structural tailwinds on his side. Nearly $20 billion of debt inflows largely linked to JPMorgan Chase & Co’s inclusion of India in its flagship emerging markets bond index has allowed officials to mop up hard currency, while bullish investors bet big on the world’s fastest growing major economy, helping its stock market overtake Hong Kong to become the world’s fourth largest this year.

India’s current account deficit has also narrowed recently thanks to cheaper oil from Russia and global firms setting up service hubs to tap growth in the nation of 1.4 billion people.

With the rupee on an even keel, the RBI is now in a position to follow the Fed and lower interest rates as inflation moderates toward its 4% target. While a cut may still happen this year, navigating the easing cycle and maintaining the hard-won currency stability may end up in a successor’s hands.

There’s no indication yet who might succeed Das, when an announcement will come, or whether he’ll get another extension.

“They’ve been successful in achieving their objectives and in a sense ringfencing India to some of the external shocks,” said Sonal Varma, chief economist, India and Asia ex-Japan at Nomura Holdings Inc. “The strategy of building fx reserves can and should continue.”

Das, a former career bureaucrat, has frequently referred to the stockpile as an “umbrella.” The rationale for the rainy day fund is to allow India to avoid a repeat of the 2013 “Taper Tantrum,” when investors bracing for a paring of US stimulus triggered the country’s worst currency crisis in two decades.

The RBI did not respond to an email from Bloomberg seeking comment on its exchange rate policy.

Due to its forays into the market, India landed on the Trump administration’s watch list for currency manipulators in 2018, and again in 2020. The International Monetary Fund also took the country to task, saying last December that management of the rupee had gone so far as to no longer make it a floating exchange rate.

The RBI “strongly disagreed” with that assessment, the Washington-based lender said. Das pushed back while at an IMF-World Bank meeting in Morocco last year, saying the US practice of putting emerging markets countries on a watchlist failed to take into account the challenges they face.

“This policy is not without shortcomings – exceptional stability can disincentivise hedging, making the exchange rate susceptible to unexpected external shocks,” said Dhiraj Nim, economist and foreign exchange strategist at ANZ Group Holdings Ltd. “However, at present, it does seem that benefits are outweighing costs.”

Those pluses include helping make Indian financial assets attractive to global funds and facilitating the government’s ambition for overseas trade increasingly to be denominated in rupees. Boosting exports — including of items like semiconductors that are crucial to Modi’s dream of having a $500 billion electronics sector by the end of the decade — is another advantage.

“The currency has been on a gradual depreciation bias over the past few quarters, to adjust for external imbalances and inflation-adjusted moves of key trading partners,” said Radhika Rao, a senior economist at DBS Group Holdings Ltd.

Steering a steady course on the exchange rate and forestalling capital flight also has implications for stability of the financial system, another of Das’s policy objectives. Earlier this year, authorities practically shut down a large part of the currency futures market in a bid to crack down on speculators. They’ve also stamped out arbitrage opportunities via offshore markets by intervening in the non-deliverable forwards market in centers like Singapore.

“The currency can come under sudden pressure if there is no safeguard,” said R Gandhi, who served as an RBI deputy governor between 2014 and 2017. “India should continue to accrue more reserves, not only to fight the volatility, but also to improve the import cover to give more strength to the economic fundamentals of the country.”